According to Experian’s State of the Automotive Finance Market Report, one reason for the downward trend in new vehicle sale smay be the rise in loan amounts, monthly payments and interest rates for new vehicles. In fact, average new vehicle loan amounts and monthly payments recently hit record highs.

According to Experian’s State of the Automotive Finance Market Report, one reason for the downward trend in new vehicle sale smay be the rise in loan amounts, monthly payments and interest rates for new vehicles. In fact, average new vehicle loan amounts and monthly payments recently hit record highs.

Findings show the average new vehicle loan hit $31,455 in Q1 2018, an increase of $921 from the previous year. The monthly payment for a new vehicle climbed to $523, a $15 increase over the same period. The average interest rate for a new vehicle was 5.17 percent during the quarter.

“The dream of owning a new vehicle is becoming more elusive to the average American,” said Melinda Zabritski, Experian’s senior director of automotive financial solutions. “To reverse the trend, dealers and lenders need to better understand the data and explore different options to make new vehicle ownership accessible and appealing.”

The report also spotlights that loan terms for new vehicles have also increased during the quarter (slightly above 69 months). While 72-month loans remain the most common loan term, more new loans have spilled into the 85- to 96-month bucket.

The population segments most impacted are subprime and deep subprime consumers. The percentage of new vehicle loans to subprime and deep subprime consumers has decreased 8.4 percent and 14.1 percent, respectively. The percentage of new vehicle loans to prime and super prime consumers has reached 73.4 percent, the highest Q1 level since 2012 – a sign that some lenders have become more risk-averse.

Delinquencies trend down; evidence of a strong loan market

While some lenders have reduced loans to riskier borrowers, the overall automotive loan market shows signs of improvement. The percentage of 30-day delinquencies have dropped 3.1 percent to 1.90 percent in Q1 2018, while 60-day delinquencies have remained flat at 0.67 percent.

“Traditionally, lenders’ risk tolerance has swung back and forth like a pendulum, and right now we’re seeing a more risk-averse side. But if payments continue to improve, we could see credit standards loosen,” Zabritski continued. “The more insight lenders have into consumer credit behavior, the better decisions they can make.”

Additional findings include:

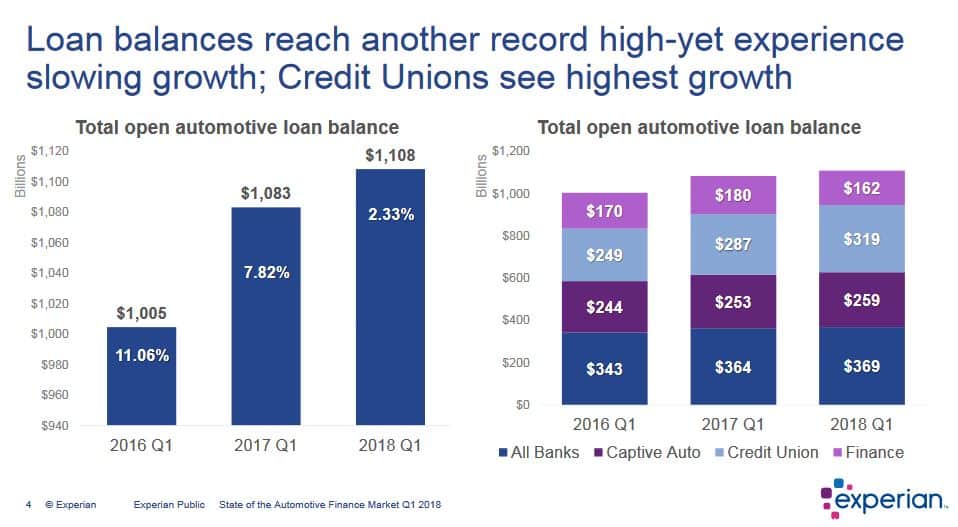

- Outstanding loan balances reached a record high of $1.108 trillion

- Credit unions continue to see the highest growth in automotive loan market share, reaching 21.3 percent, a 6.9 percent increase from a year ago

- The average credit score for a new vehicle loan rose to 716 in Q1 2018, while the average credit score for a used vehicle loan rose to 655 during the same period

- Loans for used vehicles reached $19,536 in Q1 2018, a new record high.

To view the State of the Automotive Finance Market report webinar, visit https://www.experian.com/automotive/automotive-webinars.html.